Example 14

Determine a borrower’s NAR in a deferred settlement scheme

Expanding on Example 13, this example shows how to compute the borrower’s Nominal Annual Rate (NAR) of interest, similar to the IRR, in a deferred settlement scenario. Note that since payments factor in the deferral, the calculated NAR, based on the documented date, will likely be lower than the lender’s rate, as discussed in Example 15.

This example demonstrates usage of the Deferred Settlements calculator feature to illustrate how a lender can calculate the Nominal Annual Rate (NAR) of interest implicit in a repayment profile containing payments that already take into account the deferral of a supplier settlement. In Example 14, we illustrated how a Lender calculates this unknown payment value under a deferred settlement arrangement. In Example 15, we’ll show how a lender can confirm the Nominal Annual Rate (NAR) of interest implicit in a repayment profile aligns with the original yield used to calculate the unknown payment value.

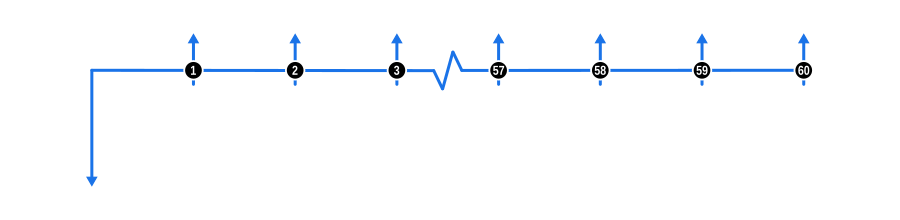

The Deferred Settlement feature is designed specifically for use by Finance Professionals, though the example should be informative for all users. The diagram below visualises the cash flow dynamics:

Example Calculation Inputs

- Advance: The cost of the goods (advance) is shown as a blue downward arrow. As this cash flow diagram shows the financial arrangement from the Borrower’s Perspective, the arrow is positioned at the beginning of the timeline.

- Payments: The known payments are represented by blue upward arrows. In the calculator, enter the result obtained in Example 13 into the payment fields.

- Interest Rate: As this is what we are solving, clear the calculator input field.

In the calculator input screen, at the foot of the Advances section, is a dropdown to select the perspective to use in solving the unknown interest rate. As we are determining the NAR from the Borrower’s Perspective, ensure that option is selected so the calculation is performed with reference to the Documented Date.

Note

We are describing the calculation of the implicit rate using the above approach as it is likely the calculator Display Settings are already set up and were used to calculate the unknown payment in the previous example. You can of course determine the implicit interest rate separately using the default calculator configuration as demonstrated in Example 16.

Benefits and Implications

- Transparency: This calculation provides borrowers with a clear understanding of their effective interest rate, fostering transparency in financial dealings.

- Comparison: Helps in comparing different financing options by understanding the true cost of borrowing under deferred settlement terms.