Dive into the heart of financial calculations with this section of the guide. Here, we unpack several pivotal financial concepts, illustrating how they’re woven into the fabric of Curo Calculator. Explore these essential topics:

Day Count Conventions: Grasp the significance of how days are counted in financial calculations. Learn about key conventions like 30/360 for standard loan calculations, Actual/Actual for precision over long terms, and Actual/365 for short-term finance. Understand when to apply APR conventions for consumer credit, and how EAR conventions annualise rates for broader applicability.

Interest Rates: Delve into the nuances of interest calculations with Nominal Annual Rate (NAR) as the basic yearly rate, Effective Annual Rate (EAR) which accounts for compounding, and Annual Percentage Rate (APR) which includes additional borrowing costs like fees, providing a legal standard for comparing loan costs. Understand how the day count convention you select influences which rate type is used in your calculations.

Modes: Understand how the timing of payments within a period affects your calculations. Learn to differentiate between In Advance (payments at the start of periods) and In Arrears (payments at the end), and see how consistent or mismatched modes across multiple payment or charge rows influence cash flow patterns.

Schedules: Explore the Amortisation Schedule for a clear breakdown of loan payments, showing how each instalment reduces principal and pays interest, ideal for financial accounting. Alternatively, the EAR/APR Proof schedule validates the calculated interest rate by ensuring discounted cash flows balance to zero, crucial for rate accuracy verification. Both schedules can be downloaded in XLSX format, with options to view day count factors for deeper analysis.

Embark on this journey through Curo Calculator’s core concepts to enhance your financial acumen and make the most of your calculations.

Subsections of Core Concepts

Day Count Conventions

Quick Version

A Day Count Convention is essentially a method of counting days for financial calculations. It might sound complex, but it’s really just about counting days in different ways.

Choosing the right convention for your calculation can be confusing due to the various options available. However, most loan repayment calculations use a limited subset of conventions available in Curo Calculator, with others reserved for more specialised scenarios. If you’re looking for guidance on which to use, here are our recommendations:

Solving unknown values and implicit interest rates:

For calculations with repayments in months or multiples of months, use 30/360. This convention is often considered the de facto standard for many financial calculations and has been in widespread use for decades.

For calculations with repayments in weeks or multiples of weeks, opt for Actual/365 or Actual/Actual. Avoid conventions based on a 30-day month as these might yield unexpected results due to how they handle periods spanning month ends.

Solving unknown APRs and unknown values using an APR:

For users in the European Union (EU), use the built-in EU 2023/2225 APR convention.

For users in the United States (US), use the built-in US Appendix J APR convention.

For users in the United Kingdom (UK), select the UK Mortgage APR for credit agreements secured on land or UK Non-Mortgage APR for those not secured on land.

For users located elsewhere, choose conventions with the EAR (Effective Annual Rate) suffix, e.g., 30/360 EAR. These conventions often mirror legally defined APR methods, providing a good proxy. If your jurisdiction has a mandated APR convention, please let us know, and we’ll consider adding support in a future release.

Continue reading for a deeper understanding of Day Count Conventions in general.

Deep Dive Version

All conventions supported by Curo Calculator are listed below, each with details to help you select the most appropriate one for your needs.

Each standard convention has a counterpart EAR (Effective Annual Rate) convention, which isn’t described separately as they use the same method of counting days. They differ only in where they start the day count from; in standard conventions, the count is based on the duration between the current and previous cash flow. In the EAR version, the count is the duration between the current and the initial advance or drawdown. This method effectively annualises the interest rate.

Info

If you work with spreadsheets, you might be familiar with the IRR (Internal Rate of Return) and XIRR (eXtended Internal Rate of Return) functions. The good news is Curo Calculator produces identical results when you solve for the unknown rate using 30/360 for IRR calculations, and Actual/365 EAR or Actual/Actual EAR for XIRR calculations!

One final point: No matter which convention you use, it’s very easy to inspect the day counts applied to each cash flow in a repayment schedule. This way, you can sense-check if your chosen convention is working as expected. For further information, see Core Concepts > Schedules.

Here are the supported conventions:

EU 2023/2225 APR

Description:

This convention expresses time intervals in years, months, or weeks, considering the frequency of drawdowns and payments.

Mathematical Logic:

When intervals can’t be expressed in whole periods, the remaining days are calculated backwards from the cash flow date to the initial drawdown, divided by 365 (or 366 in a leap year).

Use Cases:

Mandatory for computing the Annual Percentage Rate of Charge (APRC) for Consumer Credit in the EU.

Historical Context:

Implemented with the EU’s Consumer Credit Directive 2023/2225.

Example:

Weekly: From January 1 to February 4 would be counted as 5 weeks (divided by 52 weeks in a year).

Monthly: From January 1 to March 1 would be counted as 2 months (divided by 12 months in a year).

US Appendix J APR

Description:

This convention calculates the Annual Percentage Rate (APR) for closed-end credit transactions using the actuarial method, where time intervals are determined by the user-selected repayment frequency (e.g., weeks, months, or multiples thereof), with any remaining days counted as a fraction of a year.

Mathematical Logic:

Intervals are measured based on the repayment frequency chosen by the user:

For weekly payments, intervals are counted in weeks (divided by 52 for the year fraction).

For monthly payments, intervals are counted in months (divided by 12 for the year fraction).

For other frequencies (e.g., semi-monthly or multiples of weeks/months up to one year), the unit-period is the most frequent common period in the transaction.

If the interval includes a partial period (odd days), the remaining days are counted as the actual number of 24-hour intervals between dates, divided by 365, regardless of leap years.

The day count starts from the transaction’s consummation date (or when the finance charge begins, if later) to each cash flow, using the actuarial method where the unpaid balance is increased by the finance charge and decreased by payments at the end of each unit-period.

Use Cases:

Mandatory for calculating the APR for consumer credit agreements in the United States, including loans, credit cards, and other closed-end credit transactions, as required by Regulation Z of the Truth in Lending Act (TILA).

Historical Context:

Established under Appendix J of Regulation Z, part of the U.S. Truth in Lending Act (TILA), to standardize APR calculations for consumer transparency, effective since the TILA’s enactment in 1968 and refined through subsequent amendments.

Example:

Weekly: For a transaction from January 1 to February 5 (35 days, or 5 weeks), the interval is counted as 5/52 years, with no odd days if payments align weekly.

Monthly: For a transaction from January 1 to March 10 (68 days), if monthly payments are selected, the interval is counted as 2/12 years (for two months) plus 10/365 years (for the remaining 10 days).

UK Mortgages APR (UK CONC App 1.1)

Description:

This convention is used for calculating the Annual Percentage Rate of Charge (APRC) specifically for consumer credit agreements secured on land in the United Kingdom.

Mathematical Logic:

Periods are measured in whole calendar months or weeks when possible. For periods that don’t align with whole months or weeks, time is converted into years and days.

Whole months or weeks are converted to years; any remaining days are expressed as a fraction of a year based on the year’s actual number of days (365 or 366 for leap years).

Use Cases:

Essential for mortgages and other credit agreements where the security is land in the UK.

Historical Context:

Derived from the UK’s Financial Conduct Authority (FCA) Consumer Credit sourcebook (CONC), specifically Appendix 1.1.

Example:

If a period spans from January 1 to April 1, it would be counted as 3 whole months (divided by 12 for the year fraction), or if from January 1 to January 29, it might be considered as 29 days (divided by 365 or 366 for a year fraction).

UK Non-Mortgages APR (UK CONC App 1.2)

Description:

This convention applies to calculating the Annual Percentage Rate of Charge (APRC) for consumer credit agreements not secured on land in the United Kingdom.

Mathematical Logic:

Time intervals between dates are calculated directly in years or fractions thereof.

A year can be viewed as having 365 days (or 366 in leap years), 52 weeks, or 12 equal months.

For irregular periods, the time is converted into a fraction of a year based on the number of days in the year (365 or 366 for leap years).

Use Cases:

Applicable for various forms of consumer credit like loans, credit cards, etc., where no land is involved as security.

Historical Context:

Also part of the UK’s FCA CONC sourcebook, with specifics in Appendix 1.2.

Example:

From January 1 to January 31 would be 31 days, considered as a fraction of 365 (or 366 in a leap year) for the year. If from January 1 to March 1, it would be counted as 2 months (divided by 12 for the year fraction), or alternatively, as 59 days.

30/360 Convention

Description:

Assumes each month has 30 days and each year has 360 days for simplified calculations.

Mathematical Logic:

Days are calculated as if every month ends on the 30th, regardless of actual days.

Use Cases:

Preferred for bonds, fixed income, and standard loan calculations for its simplicity.

Historical Context:

Developed for manual calculations before widespread computer use.

Example:

Interest from January 1 to March 1 counts as 60 days (2 months x 30 days).

Actual/Actual (ACT/ACT) Convention

Description:

Uses the actual number of days between dates and accounts for leap years.

Mathematical Logic:

Counts every actual day, dividing by the year’s actual number of days (365 or 366).

Use Cases:

Essential for precise interest calculations in government bonds and long-term securities.

Historical Context:

Chosen for markets requiring accuracy over long periods.

Example:

From January 1, 2024, to January 1, 2025, would be 366 days if it’s a leap year.

Actual/365 (ACT/365) Convention

Description:

Counts actual days but uses a fixed 365-day year, ignoring leap years.

Mathematical Logic:

Interest is calculated over actual days but with a constant year length.

Use Cases:

Used in money markets, commercial loans, where leap years are less critical.

Historical Context:

Designed for consistent annual rate calculations in short-term finance.

Example:

From January 1 to June 1 counts over 365 days, regardless of leap years.

Actual/360 (ACT/360) Convention

Description:

Employs actual days but assumes each year has 360 days for calculations.

Mathematical Logic:

Results in higher annualised rates due to the smaller denominator.

Use Cases:

Common in U.S. banking for short-term debt where a higher annual rate is acceptable or required.

Historical Context:

Adapted from European practices for U.S. markets.

Example:

From January 1 to January 31 counts as 31 days over 360, leading to a higher annual percentage rate compared to 365 or 366 days.

Interest Rates

Quick Version

Curo Calculator is designed to solve unknown values using one of three rates of interest: a Nominal Annual Rate (NAR), an Effective Annual Rate (EAR), and an Annual Percentage Rate (APR). It also solves for an unknown interest rate when all other inputs are provided.

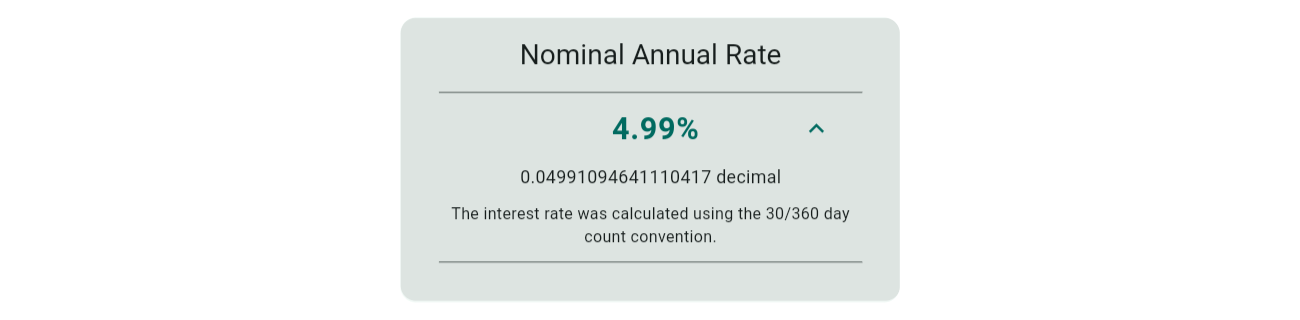

The type of interest used in a calculation is determined by your choice of day count convention. See Core-Concepts > Day Count Conventions for details on supported conventions. When selecting a convention on the calculator input screen, you’ll notice the label of the interest rate input field updates to reflect the type of interest that will be used.

Nominal Annual Rate (NAR) - The basic interest rate over a year without considering compounding or inflation.

Effective Annual Rate (EAR) - Takes into account the effect of compounding within the year, giving a more accurate annual rate.

Annual Percentage Rate (APR) - Similar to EAR in calculating days with reference to the initial drawdown but mandated by law to reflect the true cost of borrowing, including fees and other charges, but not considering compounding frequency within the year.

Deep Dive Version

Nominal Annual Rate (NAR)

Definition: The NAR is the stated interest rate for a year, before adjustments for compounding or inflation. It’s the simplest form of expressing interest.

Example: If a loan has a NAR of 5%, this means you would pay 5% of the principal in interest over one year, if no compounding is applied.

$$ Interest = Principal \times \frac{NAR}{100} $$

Effective Annual Rate (EAR)

Definition: The EAR accounts for the effects of compounding within the year. It’s the actual rate you would pay or earn annually, considering how often interest is compounded.

Example: For a nominal rate of 5% compounded quarterly:

Definition: The APR is a standardised measure of the cost of borrowing, mandated by law to reflect not just the interest rate but also other charges like fees, providing a more comprehensive view of borrowing costs. However, unlike NAR, it does not account for the frequency of compounding within the year.

Example: Consider a one-year loan of €1,000 where:

The Nominal Annual Rate (NAR) is 5%.

The loan has an origination fee of 1% (€10 added to the cost).

Interest compounds monthly, but for simplicity, we’ll calculate APR assuming annual compounding for comparison with regulatory standards.

Calculating APR:

Total Interest: Based on NAR, the interest would be €1,000 * 5% = €50.

Total Fees: The origination fee adds €10.

Total Cost of Borrowing: €50 (interest) + €10 (fee) = €60.

For APR:

Simplified APR Calculation (assuming annual compounding for regulatory purposes):

This means, although the NAR is 5%, when you include the fee, the APR effectively becomes 6%, providing a clearer picture of the loan’s cost without considering the compounding effect within the year.

Modes

A mode determines when an amount is due within the period defined by a chosen frequency. With a mode set to In Advance, the amount becomes due at the start of the first period, and in any subsequent periods within a cash flow series. When set to In Arrears, the amount is due at the end of the first and subsequent periods.

Note

When set to In Advance, a single payment or charge is automatically assigned a One-off frequency, occurring as a single event without recurring periods. This aligns the cash flow with the contract start date or the end date of a prior series for improved readability. Explore this feature in examples 02, 05, and 11.

The Mode selection is only displayed when date input is disabled, a topic covered in Settings > Display > Date Input. When dates are in use, you have full control over when the first amount in a series falls due.

Modes with Multiple Rows

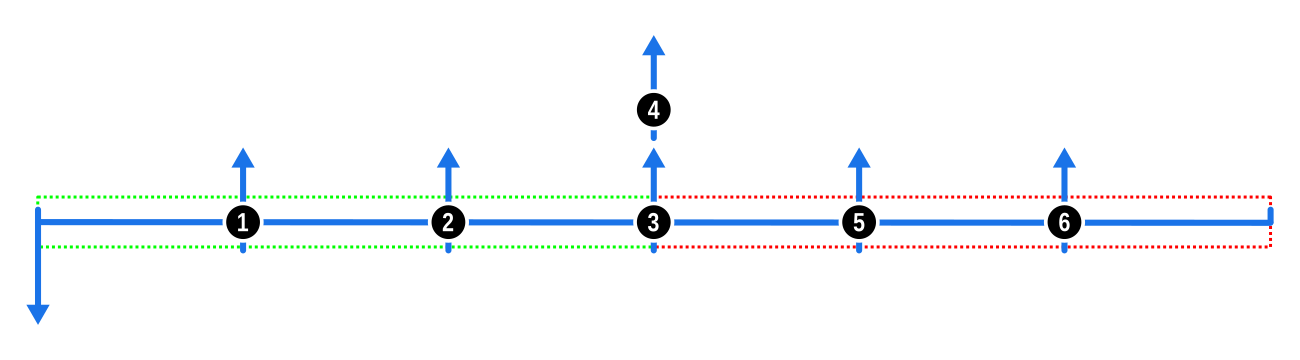

When performing calculations with more than one Payment or Charge, the mode you select in each row applies only to that row. To avoid unexpected results from mismatched modes, as described below, you should aim for consistency by using the same mode across all Payment or Charge rows.

The first diagram illustrates the consistent application of the In Advance mode across two payment series, resulting in equal spacing of cash flows. This spacing would be similar if both were set to In Arrears.

The next diagram shows the effect when the first payment series is set to In Advance and the second to In Arrears. The mismatch results in a gap, the width of which is equal to the frequency of each series.

Conversely, the following diagram depicts what happens when the first payment series is In Arrears and the second is In Advance. Here, the final payment in the first series coincides with the first payment of the second.

Keep these points in mind when selecting modes across multiple rows to ensure your calculations align with your expectations.

Schedules

Curo Calculator offers two distinct types of schedules: the Amortisation Schedule and the EAR/APR Proof. The choice of day count convention you make on the input dictates which schedule will accompany your calculation results, accessible on the second tab of the results screen. Here’s the breakdown:

Amortisation Schedule: Generated for all standard day count conventions (e.g., 30/360, Actual/Actual), this schedule details each payment on a loan, showing how each instalment is split between interest and principal reduction. This is particularly beneficial for business borrowers who need to update their financial accounts with precise payment allocations.

EAR/APR Proof: Produced when using conventions with an EAR or APR suffix (e.g., US Appendix J APR, EU 2023/2225 APR), this schedule demonstrates the calculation methodology behind the rate and verifies its accuracy by ensuring that all discounted advances, payments, and charges net out to zero. It’s invaluable for both lenders and borrowers who need to validate or dispute the interest rate applied to a loan.

From a Curo Calculator perspective, these schedules serve to:

Present results in an easily digestible format.

Allow you to quickly sense-check if your calculation inputs yield the expected repayment profile, particularly in complex scenarios with multiple variables.

Enable validation of an interest rate result when necessary.

All schedule data can be downloaded in XLSX (spreadsheet) format for your records or further analysis. Simply click the download button at the top of each schedule.

When a schedule contains same-dated payments, a Bundle Payments button appears at the top. Toggle this button to bundle or unbundle same-dated payments for a cleaner, more organized display. Explore this feature in examples 07 and 09.

The following section delves into how to validate any interest rate result produced by Curo Calculator using the data provided in these schedules. This part gets quite technical and might primarily interest those seeking a deep dive.

Interest Rate Validation

EAR/APR Proof

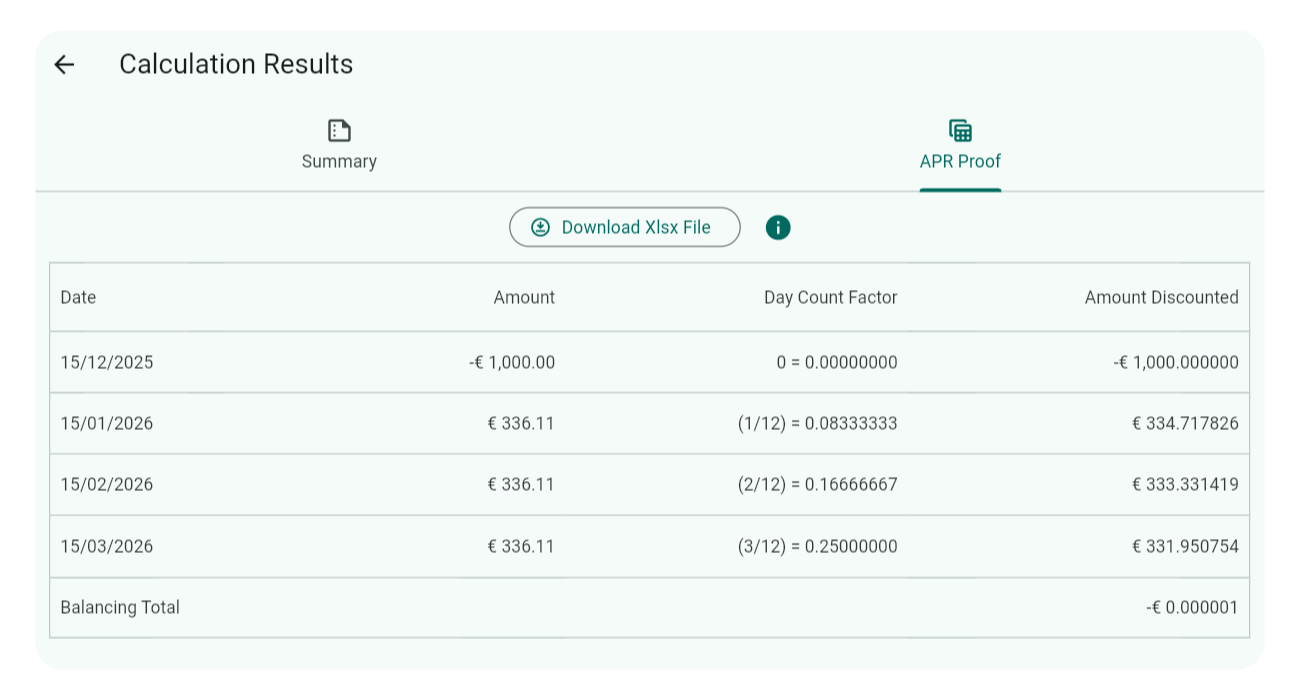

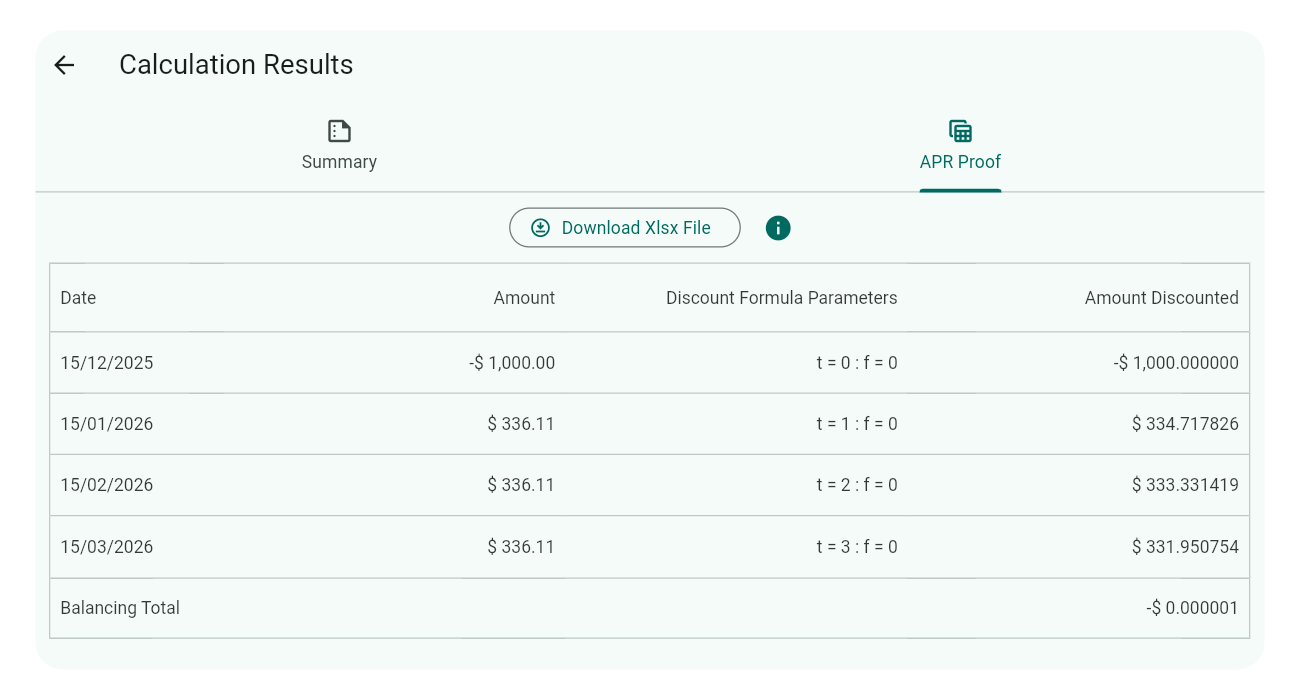

The EAR/APR Proof schedule uses one of two discount approaches to validate the interest rate, depending on the selected APR convention:

Standard APR Conventions (e.g., EU 2023/2225 APR): These use a standard discount formula and display a Discount Inputs column with the factor ( $t$ ) for each row.

US Appendix J APR: This uses a U.S.-specific discount formula, reflecting the actuarial method, and displays a Discount Inputs column with parameters ( $f$ ), ( $t$ ) and ( $p$ ) for each row.

Below, we provide a simplified example for each approach to illustrate the validation process.

Standard APR Conventions

For standard APR conventions, the proof schedule includes a Discount Inputs column showing ( $t$ ), the time factor for discounting. Below is an example schedule:

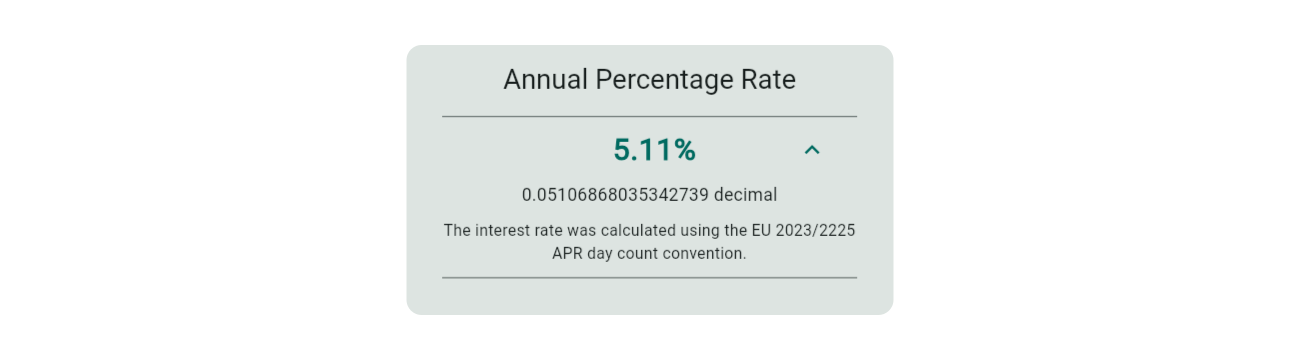

The interest rate to validate is found under the result summary tab:

To prove the interest rate (5.11%) is accurate, discount each value in the Amount column using the Discount Inputs ( $t$ ) and the annual interest rate (as a decimal), then sum the results. The discount formula and example calculations are provided below:

Standard APR discount formula

$$ d = a \times (1 + i)^{-t} $$

where:

( $d$ ) = Amount Discounted

( $a$ ) = Amount (to be discounted) from the schedule

The Balancing Total column maintains a running total that should reduce to zero, though minor variations (±0.01) may occur due to rounding. Here, the total is -0.00, confirming the interest rate of 0.05106868 (5.11%) is correct for the EU 2023/2225 APR convention.

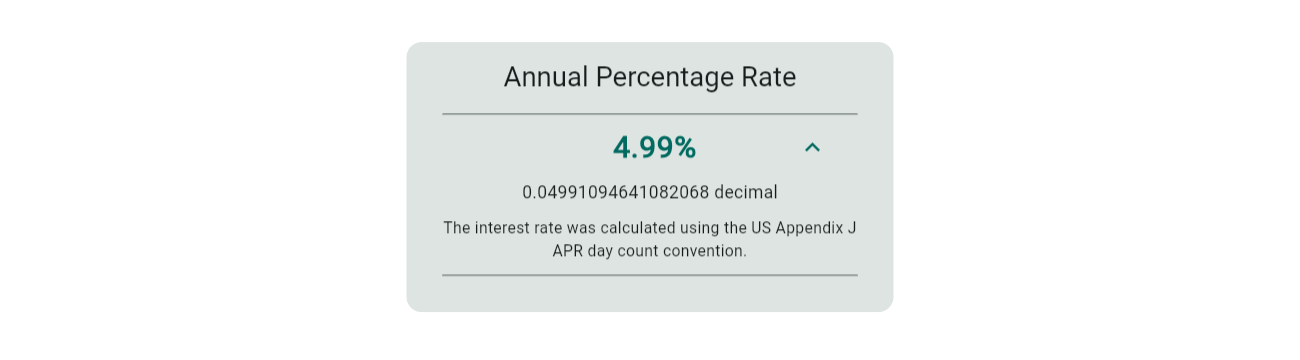

US Appendix J APR

For the US Appendix J APR convention, the proof schedule includes a Discount Inputs column showing ( $f$ ) (odd-days factor), ( $t$ ) (unit-period time factor) and ( $p$ ) (unit-periods in a year). Below is an example schedule for a loan with three monthly repayments:

The interest rate to validate is found under the result summary tab:

To prove the interest rate (4.99% annual) is accurate, discount each value in the Amount column using the Discount Inputs ( $f$ ), ( $t$ ), ( $p$ ) and the annual interest rate ( $i$ ) (expressed as a decimal), then sum the results.

The discount formula and example calculations are provided below:

US Appendix J APR discount formula

$$ d = \frac{a}{(1 + f\frac{i}{p})(1 + \frac{i}{p})^t} $$

where:

( $d$ ) = Amount Discounted

( $a$ ) = Amount (to be discounted) from the schedule

The Balancing Total column maintains a running total that should reduce to zero, though minor variations (±0.01) may occur due to rounding. Here, the total is -0.00, confirming the annual interest rate of 0.04991094 (4.99%) is correct for the US Appendix J APR convention.

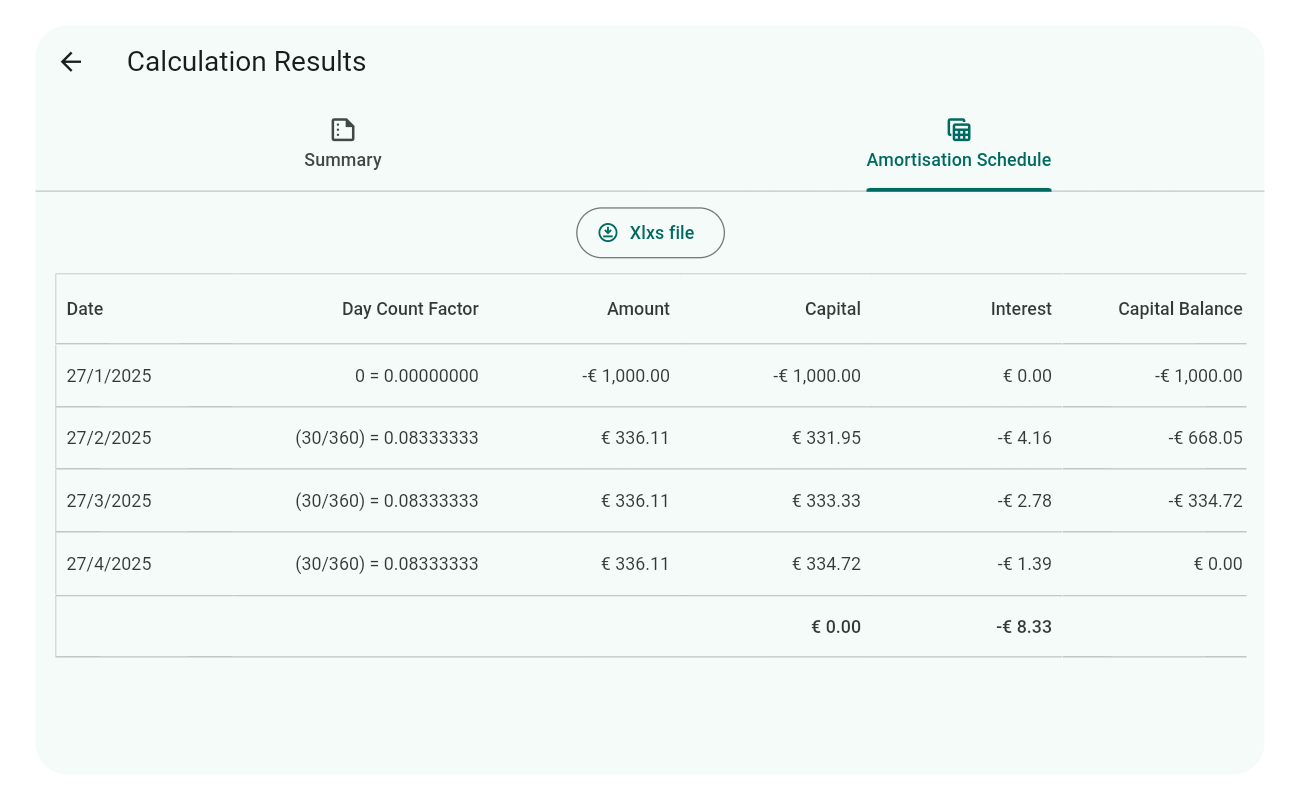

Amortisation Schedule

To validate the interest rate, we offer a simplified example of an amortisation schedule in the image below:

Notice the additional column after the Date column, which shows the Discount Inputs applied to each row. This column is hidden by default because day count factors can be confusing. To view it, tap or click 3 times on the Date column title. Repeat to hide it again.

The interest rate you need to validate can be found under the result summary tab:

To confirm that the interest rate of 4.99% (as shown above) is accurate, you need to calculate the periodic interest for each row. Add this interest to the capital balance brought forward and the amount to determine the capital balance carried forward. Repeat this for each row until you reach the end.

Here’s the formula for periodic interest, followed by the step-by-step workings:

In amortisation calculations, the final Capital Balance should ideally be zero, with minor deviations permitted due to rounding errors, thus proving the interest rate of 0.04991095 (4.99%) correct for the chosen 30/360 day count convention.

Tip

Even if you’re not interested in validating the interest rate, uncovering the Discount Inputs column can be helpful to see how the day counts are used in the calculation for your selected convention. Remember, the day count is based on the duration between the current and previous cash flow.